- The C.R.E.A.M. Report

- Posts

- Wall Streets Seasonality Hitmen...

Wall Streets Seasonality Hitmen...

The Streets Are Hunting....

Kevin Davis

December 23, 2025

Above Average Info For The Average Joe…

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - WEALTHY RED - Limited Quantities - Grab Yours Today! CLICK HERE

WEALTHY RED…

The Ridiculous Stylings Of Risky Randy Pt3…

Meet Risky Randy — patron saint of YOLO trades, lover of leverage, and sworn enemy of stop losses.

Randy believes markets exist purely for his entertainment. Every morning, he scans TikTok for “can’t miss trades,” confident that his next options play will buy him a penthouse suite (not that he’s been remotely close to one).

Market makers adore Randy. He’s the guy on the other side of every “zero days to expiration” call option that mysteriously expires worthless while Wall Street quietly pockets the premium.

Randy’s motto: “Buy higher—it’s going higher.” It’s the kind of reasoning that would make even tulip bulb speculators in 1637 blush. He’s the self-proclaimed “king of conviction,” a fearless trader armed with confidence, caffeine, and not a single functioning risk-management protocol.

When his positions go red, it’s not a warning sign—it’s “just temporary market manipulation.” When they turn green, he screenshots the gains, posts them to X, and calls himself a financial prophet.

But this, dear reader, is not a story of triumph. It’s the full-color portrait of short-term pleasure morphing into long-term pain. Because while Randy’s chasing dopamine hits from rapid-fire trades, the institutional machine is running a casino where they built the tables, deal the cards, and occasionally write the rules.

The Machine Behind the Market

Here’s what Randy doesn’t understand: markets are no longer a playing field—they’re a battlefield, and he’s walking into it with a Nerf gun.

Behind every flickering price chart sits an invisible infrastructure operated by machines that think (and react) thousands of times faster than he ever could.

High-frequency traders (HFTs) don’t see the market in minutes or even seconds—they see it in microseconds. Their algorithms analyze order flow, quote changes, and liquidity imbalances in real time.

While Randy’s hitting “buy” on his mobile app, some quant firm in Secaucus, New Jersey, has already executed, hedged, and arbitraged the same idea five times over.

While Randy’s hitting “buy” on his mobile app, some quant firm in Secaucus, New Jersey, has already executed, hedged, and arbitraged the same idea five times over.

Think of it like this: Randy’s driving a go-kart at 30 mph while Citadel’s algorithms are piloting fighter jets at Mach 2. His trades don’t even show up on their radar—except as a liquidity event to be arbitraged.

Randy believes he’s competing in a fair market, where ideas and guts determine outcomes. But he’s actually stepping into an arena designed by institutions for institutions.

Market-makers, exchanges, and hedge funds exchange information and order flow with precision that would make the Pentagon jealous.

Retail order flow—yes, including Randy’s—gets routed, categorized, and sold. It’s not personal; it’s just business. The market machine knows which orders are impatient, which are likely to panic, and which can be used to fill institutional needs. By the time Randy “feels bullish,” the price move he’s reacting to may already be priced in.

Meanwhile, large institutions operate on an entirely different information grid. They don’t watch CNBC for clues—they are the clue. They see sector rotation via dark pools before anyone else sees it on a chart.

They receive corporate tone analysis, supply-chain data, and credit conditions weeks or months before the average trader reads about them online. When the Fed hints at a pause, Randy hears it at lunch. Hedge funds hear it in the data.

What keeps Randy in the game isn’t logic—it’s dopamine.

Every time a trade works for a few minutes, his brain lights up like a slot machine. Each win reinforces belief in skill rather than chance. And every loss gets rationalized away—bad luck, bad timing, bad Fed. Never bad strategy.

He’s not alone. The short-term trader’s mindset is built on an illusion of control. When prices flash green or red, the brain interprets it as action resulting in consequence—like pushing a button and receiving a reward. But markets don’t work like that. They’re largely random in the short term, driven by liquidity, vol events, and positioning—not “vibes” or conviction.

Over time, this chase for immediate satisfaction rewires behavior: the more trades made, the more volatile the emotions, and the less capable the trader becomes at rational decision-making. In psychology, it’s called variable reward reinforcement — the same mechanism casinos use to keep gamblers glued to slot machines.

Institutions don’t trade for quick pleasure. They scale in, hedge out, hold patience as a strategic asset, and use data models that retail traders can’t dream of matching. They run stress tests, scenario analyses, and have access to leverage at interest rates Randy’s broker would never offer.

They buy risk, but they manage it — all while Randy burns through his brokerage account with the finesse of a fireworks show at a gasoline station.

Capital is their weapon. Algorithms are their shield. Information is their intelligence network. Retail psychology? That’s their edge.

Risky Randy doesn’t stand a chance—not because he’s dumb, but because he’s human in a market increasingly inhuman. He’s chasing certainty in a game engineered to exploit emotion and impatience.

Every “all-in” trade is just another donation to the liquidity gods. Every overconfident click is another laugh for the market makers who already know how the game ends.

If Randy really wants to win, he must learn to stop playing their game. Patience. Risk management. Discipline. Long-term compounding. These are the weapons institutions built their empires on—and the very ones Randy trades away for the thrill of being “right” in the moment.

Short-term pleasure is long-term pain. But if Randy finally learns to step back, think bigger, and stop trying to beat the bots at their own game, he might discover that the slow, boring way is the only truly profitable one.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BILL GATES BLACK - Limited Quantities - Grab Yours Today! CLICK HERE

Wall Streets Seaonality Hitmen…

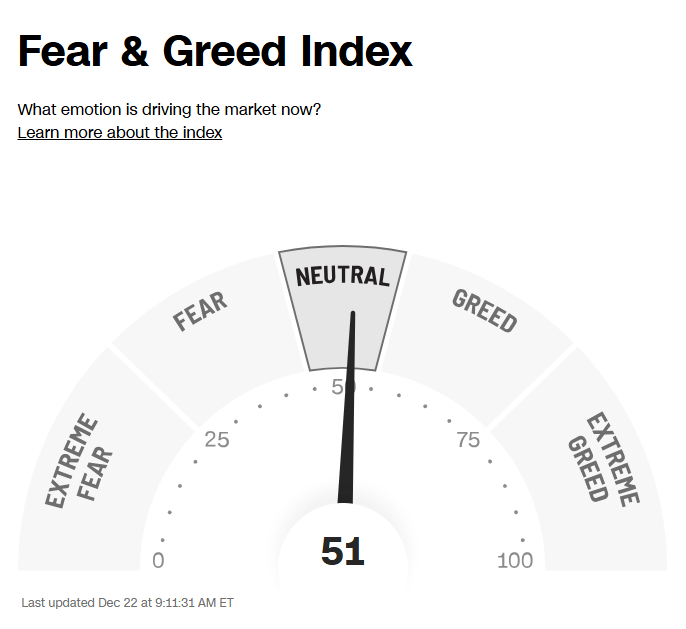

It was the season of joy — unless you were the kind of investor who still believed markets moved on fundamentals alone. This year, Wall Street’s favorite character returned to the stage: the seasonality hitman – part options dealer, part narrative engineer, full-time liquidity extractor.

The timing, as usual, was exquisite. AI euphoria at full blast, option books bloated, and retail finally buying the dip with both hands. Then came the big set piece: quadruple witching, rebranded in headlines as if it were financial Armageddon.

Quadruple witching, for the lucky few who still sleep at night, is when four types of derivatives expire together: stock index futures, index options, single-stock options, and single-stock futures, typically on the third Friday of March, June, September, and December.

On those days, volume doesn’t just rise — it detonates. Historical data show SPY and index volume can run at multiples of normal, with the final hour of trading often seeing truly absurd flows as funds roll, rebalance, or just panic-flat their books.

In other words, it’s not “random chaos.” It’s a scheduled harvest.

AI bubble, or AI buffet?

On the surface, this was the year of the “AI bubble.” Commentators warned that the whole market was being levitated by one ticker symbol in particular: NVIDIA. The joke was that every earnings report sounded like a science-fiction sequel with a bigger budget.

But beneath the hysteria, the numbers were inconveniently strong. NVIDIA posted year-over-year revenue growth north of 50% multiple quarters in a row, including roughly 56% and 62% gains in back-to-back periods, with quarterly sales in the tens of billions.

At the same time, worries about an “AI bubble” became a media genre of their own, even as the company repeatedly beat expectations and raised guidance.

So was it a bubble? For the narrative hitman, that question was irrelevant. What mattered was that “AI bubble” made a great headline on the way down, and an even better justification for performance-chasing on the way back up.

Quadruple witching and the fear machine!!!

Then came the apocalyptic quadruple witching promos. Estimates pegged some individual witching days with notional options exposure above $7 trillion, with S&P 500 trading volume spiking to the highest levels of the year on those sessions.

Backtests show the pattern: quadruple witching days tend to be volatile with lower average returns, while the week around them can be oddly strong, followed by weaker performance in the week after.

You don’t need a tinfoil hat to see the incentives. When volume explodes and options, futures, and index products all expire at once, market makers are not “victims of volatility” — they are the toll collectors. Data show that on these days, SPY and major ETFs often trade at far above their 30‑day average volume, with the closing auction acting as a liquidity bonfire.

Layer on top a media cycle built on maximum emotional beta. A modest rate hike or policy tweak from the Bank of Japan is suddenly framed as the trigger for a global “carry trade unwind” and systemic risk, even when underlying moves in rates are incremental. The story is always the same: volatility is treated as a shock, not as a scheduled opportunity.

Narrative as a weapon: rotation, fear, and “cheap stock”

While retail investors were being told “If the Fed cuts, it means recession,” professionals were quietly doing something else: weaponizing rotation.

Under the banner of “prudence,” flows moved from AI leaders into laggards, from growth to “value,” from cyclicals to defensives — often clustering suspiciously around options expiries, macro data prints, and central bank speeches.

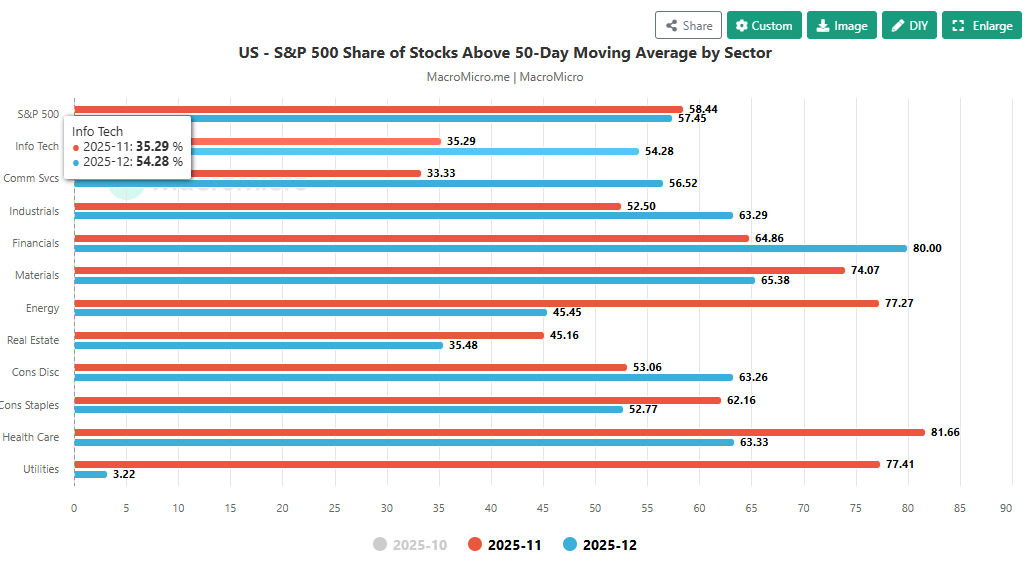

Behind the scenes, one uncomfortable reality drove much of this theater: most active managers were once again underperforming the S&P 500. SPIVA data show about 65% of active large-cap U.S. equity funds lagged the index in 2024, with similar or worse figures over many prior years. Over longer windows, the numbers get even more brutal, with the majority of stock-pickers underperforming over 10- and 20‑year horizons.

So when you see “peculiar down days” that just happen to make high‑quality names 5–10% cheaper into quarter‑end, and then watch those same names get scooped up by funds that had been lagging all year, you’re not seeing random chaos — you’re watching career risk mitigation dressed up as market wisdom.

For retail, this season felt like an extended psychological stress test. Inflation prints drifted lower, growth remained positive, and unemployment stayed historically low — a backdrop that, in any rational world, would be at least neutral for equities.

Yet every incremental sign of potential Fed easing was repackaged as a new reason to fear:

• If the Fed didn’t cut, the narrative was “policy is too tight.”

• If the Fed did cut, the narrative became “they must see something terrible coming.”

Meanwhile, the data on actual price action around these “event days” lined up more with positioning than with fundamentals: volume spikes, spread-widening, sharp intraday reversals, and then a slow grind back that rewarded those who ignored the drama and stayed long. Historical analysis around quadruple witching shows exactly this pattern: volume and volatility jump, but the structural trend often reasserts itself once the expiries are cleared.

The unsentimental verdict: the market wasn’t confused. It was simply doing what it always does — using narrative and calendar structure to strip weak hands of their shares.

Yet not everyone played victim. A subset of long-term investors treated this entire season like what it was: a live‑action reenactment of every SPIVA report ever written plus a derivatives calendar.

They understood a few simple, impolite truths:

• Most active funds, over time, lose to broad indices, especially in mega‑cap large-cap land.

• Quadruple witching routinely amplifies volume and volatility, but rarely changes the underlying fundamental trajectory of businesses.

• Companies with genuine earnings power — like the AI leaders still posting 50%‑plus revenue growth — are not magically “over” because a narrative cycle turns bearish for a month.

So while the economic hitmen emptied their seasonal magazines — volatility spikes, doom headlines, manufactured rotations — these investors simply stayed one strap ahead. They treated fear as a factor, not as a forecast. They bought when liquidity needed a counterparty.

The result? When the smoke cleared, the market, in classic fashion, had gotten exactly what it wanted from the Fed and the data — and still found new reasons to complain. The hitman got his volatility. The underperforming funds got their cheaper entries. And the patient, slightly cynical long-term investors got what they came for: more ownership of real businesses, pried loose from shaken hands at a discount.

In other words, just another season for Wall Streets hitmen.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BUY THE DIP NAVY - Limited Quantities - Grab Yours Today! CLICK HERE

BUY THE DIP NAVY…

Quick Links…

Thank you for reading, we appreciate your feedback—sharing is caring.

Reply