- The C.R.E.A.M. Report

- Posts

- Are We Selling Glass Houses...

Are We Selling Glass Houses...

It Must Be An Election Year....

Kevin Davis

January 13, 2026

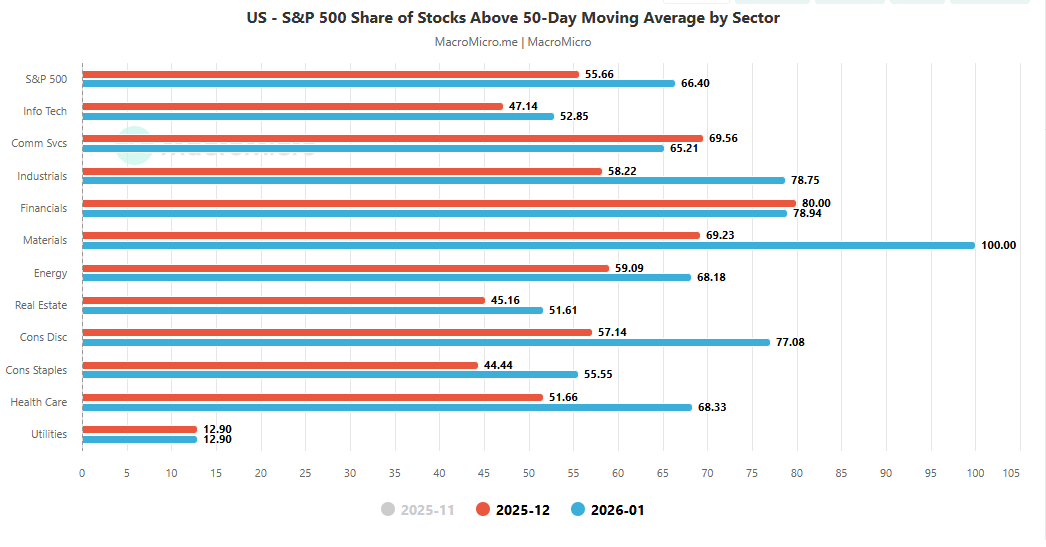

Above Average Info For The Average Joe…

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - WEALTHY RED - Limited Quantities - Grab Yours Today! CLICK HERE

WEALTHY RED…

Will China Blink…

Venezuela just went from being China’s favorite distressed high-yield oil bond to an American-controlled restructuring, and the “Nicola Montero moment” is basically the change-of-control clause kicking in on Beijing’s barrel entitlement.

What looks like a local regime shuffle is really Washington yanking away one of China’s quiet backup energy lifelines while also slamming the side door that Iran and Russia were using to dodge sanctions.

China thought it had stapled itself to Venezuela’s subsoil with oil-for-loan contracts well the US just took a legal machete to that paperwork.

• Chinese policy banks and SOEs extended roughly 60 billion dollars in loans to Venezuela, largely collateralized and repaid in crude shipments over the last decade.

• Analysts now estimate Caracas still owes around 10 billion dollars, with Chinese firms notionally entitled to about 4.4 billion barrels of reserves via project stakes and oil-for-loan structures that were meant to be worked off over many years.

• In practice, more than half of Venezuela’s roughly 750–800 thousand barrels per day of output has been quietly flowing to China, often laundered through ship‑to‑ship transfers off Malaysia and third-country intermediaries to dodge US sanctions.

That’s the “barrel entitlement” that just got subordinated. A US‑aligned government can simply declare parts of those agreements odious, reopen terms, or slow-roll repayment, instantly turning China’s secured exposure into a messy EM restructuring case.

On paper, China can shrug: Venezuelan oil was only a few percent of its total crude imports, dwarfed by volumes from Russia and Saudi Arabia. In reality, this was a strategic call option on the world’s biggest official oil jackpot.

• Venezuela holds around 303 billion barrels of proven crude reserves, the largest in the world, ahead of Saudi Arabia and Iran, plus enormous heavy-crude basins that matter if you believe in a long, messy energy transition.

• JPMorgan and other analysts think output could rise from roughly 750 thousand barrels per day to 1.3–1.4 million within a couple of years if governance stabilizes and Western majors re‑enter, with more upside later.

• For China, having preferential access to that ramp—through preexisting loans, JV stakes, and political leverage—was a hedge against any future attempt by Washington to weaponize seaborne crude flows around a Taiwan crisis.

Calling it “the move that stopped a Taiwan invasion” is hyperbole, but this was absolutely a backup barrel stack for Beijing: cheap heavy crude outside the Strait of Hormuz, contractually tied to Chinese banks, and partially insulated from US naval chokepoints.

The Venezuelan pivot does not just hit China; it rips out a sanctions-evasion node that Iran and, to a lesser degree, Russia have been using like a laundromat.

• For Iran, Venezuela was an overseas extension of its sanctions workaround: Tehran shipped gasoline, refinery parts, and technical support; Caracas paid in heavy crude, gold, and other commodities through opaque barter deals and shadow shipping.

• Iranian-linked projects in Venezuela reached an estimated 4.7 billion dollars by late 2025, centered on refinery repairs like El Palito and plans for the huge Paraguana complex—assets that now look exposed under a pro‑US administration.

• The same ghost fleet tactics and informal financial channels used to move Venezuelan barrels overlapped with those that help Iran keep 1.5–2 million barrels per day on the water despite sanctions; tightening on Venezuela raises the legal and enforcement risk around that entire ecosystem.

Russia is less structurally tied than it was a few years ago, but it still loses a friendly OPEC+ voice with the world’s largest reserves and a shared interest in pushing back on US sanctions architecture.

A Venezuelan rehab that adds another half‑million barrels per day over time chips away at Russia–Iran’s leverage inside OPEC+ just when they want tight markets to monetize their own sanctions‑discounted barrels.

Trump’s “raising” foreign policy

Strip away the moral cover, and Trump’s Venezuela play is exactly on brand: treat geopolitics like a distressed assets desk with aircraft carriers.

• The Trump administration previously used sanctions to choke PDVSA, block its assets in the US financial system, and recognize an alternative “legitimate” government to redirect those assets—effectively a hostile takeover attempt of a sovereign oil company.

• The current phase goes further: a mix of sanctions, legal pressure over oil‑for‑debt swaps, and selective enforcement against tankers has constrained Venezuelan exports and opened the door for a friendlier regime aligned with Washington’s commercial and strategic preferences.

• This signals to every petro‑autocrat that US policy under Trump is less “rules‑based order” and more “capital structure optimization with cruise missiles”: if your reserves matter, your political survival is downstream of American risk appetite.

The attitude shift matters. It tells Beijing, Tehran, and Moscow that the US is willing not just to sanction, but to physically and legally reassign flows and assets, including barrels they thought were already spoken for.

By muscling into Venezuelan politics, Washington is not just virtue-signaling about democracy; it has parked itself on a pile of long-dated collateral.

• Oil: ~303 billion barrels of proven reserves, mostly heavy, plus realistic medium‑term upside in output from ~0.75 to 1.3–1.4 million barrels per day if Western capital and technology return.

• Gas: Substantial but underdeveloped natural gas reserves with potential for LNG exports to the Atlantic basin over time, competing with Russia and complementing US LNG in Europe and Latin America.

• Metals and minerals: Significant gold reserves and other strategic minerals used as barter and collateral in past deals with Iran and others, now more open to Western legal claims and JV structures.

From a portfolio perspective, the US just converted a hostile, sanctioned mega‑reserve—used as a financing hub by China, Iran, and Russia—into a potential pro‑US, Western‑capital‑friendly asset with optionality across oil, gas, and minerals.

So yes, calling it a pure “snatch and grab” understates the sophistication. This is closer to 3‑D capital structure chess:

• Impair China’s oil‑for‑loan collateral.

• Disrupt Iran’s sanctions‑evasion plumbing.

• Soften future OPEC+ leverage from Russia and Iran by rehabilitating the one country with even more reserves.

If you’re sitting in Beijing, watching a US‑aligned government take over the one Western‑hemisphere mega‑reserve where you thought you had secured barrels for decades, you are not revising down your Taiwan ambitions because of it—but you are updating your model for how aggressively Trump is willing to weaponize other people’s balance sheets.

On the other hand Greenland is the rare‑earths and Arctic‑shipping leg of the same strategy that Venezuela represents for oil: deny China cheap, politically vulnerable supply and tighten the noose on its war‑time logistics.

The U.S looks to be cutting China’s rare earths monopolyedge:

• China controls roughly 80–90% of global rare‑earth processing capacity, which is exactly the leverage it would weaponize in any Taiwan confrontation.

• Greenland’s deposits of rare earths, uranium, and other “green” minerals are now being framed by Washington and Brussels as a way to build a parallel Western supply chain and reduce exposure to Chinese choke points.

• Trump’s renewed push to “own” or at least dominate Greenland is explicitly sold as economic and national security policy—locking in those resources before Chinese state‑linked companies can.

If Venezuela is about who controls the marginal barrel, Greenland is about who controls the magnets, chips, and batteries that make the war machine run.

• China’s Arctic strategy brands it a “near‑Arctic state,” aiming to build a “Polar Silk Road” of shipping lanes and energy projects that bypass US‑dominated chokepoints like Malacca.

• Greenland sits next to key Atlantic–Arctic routes and hosts existing US military infrastructure; more American control there means more surveillance and leverage over Arctic shipping that Beijing hoped would be a safer back door in a crisis.

From Beijing’s perspective, Washington trying to grab Greenland right after flipping Venezuela looks like a coordinated move to pre‑empt both southern (oil) and northern (minerals and shipping) workarounds.

Losing influence in Venezuela and facing US assertiveness over Greenland tells Chinese planners that alternative supply routes and non‑US‑controlled resource basins are not politically secure in a war.

That pushes them to:

• Double down on stockpiling and domestic substitution for rare earths and energy‑intensive industries.

• Accelerate Arctic and Russia‑centric routes while they still can, before the US and its allies lock more of that down.

• Treat a Taiwan conflict as something that must be short and decisive, because the US is clearly preparing to squeeze China from Venezuela to Greenland if it turns into a long grind.

So Greenland is not “about Taiwan” on the surface, but in the spreadsheet of war‑time logistics, it is another column where the US is trying to make sure China has fewer escape hatches when the Taiwan question stops being theoretical. It does not “stop” Beijing from moving on Taiwan, but it absolutely reinforces the costs and reminds Chinese planners that the US is willing to weaponize assets and sea‑borne energy in ways that directly threaten China’s war stamina.

• China’s formal line is that Venezuela is outrageous but not precedent‑setting for Taiwan; Taiwan is framed as an “internal affair,” unlike a distant Latin American client state.

• Strategically though, elites just watched the US physically grab a partner regime, threaten to redirect its oil, and shrug off Beijing’s diplomatic protests—that’s a live demo of how ruthless Washington is prepared to be in its own sphere.

So Venezuela does not rewrite the Taiwan playbook, but it sharpens every red‑ink line on the “costs” side of the ledger.

• China is already acutely aware that a Taiwan fight means energy vulnerability: it is the world’s largest importer of oil and LNG, with a majority coming by sea through US‑dominated chokepoints like Malacca and the South China Sea.

• Modeling shows that a serious interdiction could wipe out around 60% of China’s crude imports and nearly 30% of its gas (via LNG), implying something like a mid‑teens hit to GDP if fully sustained—catastrophic for the Party’s legitimacy.

Venezuela matters here because Beijing just saw one of its “alternative” oil backstops in the Western Hemisphere turned into a US‑controlled asset, which tightens that energy noose in any long war scenario.

Realistically, this pushes Beijing in three directions:

• More cautious on timelines: it reinforces that a Taiwan move has to be lightning‑fast and decided on Beijing’s terms, before the US coalition can fully mobilize its economic and energy tools.

• More focused on gray‑zone coercion: think regulatory “blockades,” Coast Guard harassment, and energy‑lifeline pressure on Taiwan designed to force capitulation without triggering the full embargo that would crush China’s own imports.

• More paranoid about overseas assets: Venezuela shows that Chinese equity, loans, and oil‑entitlement deals in US‑reachable jurisdictions are not safe in a crisis, so they look even less like reliable wartime hedges.

That combination does not kill the ambition to absorb Taiwan, but it strengthens the bias toward psychological and economic strangulation over a brute‑force amphibious D‑Day.

Bottom line: “think twice,” not “never”

• Analysts tracking Beijing’s reaction are clear on one thing: the Venezuela raid is being logged as proof that Trump will use force and legal aggression to smash Chinese interests in third countries, but it is not seen in Beijing as a green light to “retaliate” on Taiwan.

• Instead, it’s another data point telling Chinese planners that in any Taiwan scenario, the US will go straight for China’s supply lines and offshore assets—and now they have one more painful case study to plug into those wargames.

So yes, it makes China think twice—in the sense of raising perceived costs, shortening feasible war duration, and reinforcing the need for non‑kinetic coercion—but it does not remove Taiwan from the strategic to‑do list.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BILL GATES BLACK - Limited Quantities - Grab Yours Today! CLICK HERE

Are We Selling Glass Houses…

Trump’s housing “rescue” is basically a magician’s trick: yell about evil institutions, wave a $200 billion MBS bazooka at Fannie/Freddie, maybe shave mortgage rates by a few tenths, and quietly lock in even higher home prices and stickier inflation if supply doesn’t move. The policy optics are populist; the mechanics are asset-price friendly and affordability-hostile.

The setup: Trump vs “the Institutional Machine”

• Trump has said he wants to ban large institutional investors from buying additional single‑family homes, framing it as taking houses “back” for regular Americans.

• At the same time, he has ordered Fannie Mae and Freddie Mac to buy up to $200 billion in mortgage‑backed securities (MBS) using their accumulated capital, pitched as a way to push mortgage rates lower and make homeownership more affordable.

• Institutional ownership of single‑family homes is a villain with great PR value but tiny actual footprint: large institutions bought only about 0.3% of all U.S. homes sold in 2024, down ~90% from 2022 levels.

Translation: the “ban Wall Street from stealing your house” plank is mostly narrative; the real macro lever is the $200B MBS grab.

The $200B MBS buy:

Think of Fannie/Freddie as being ordered to run a mini-QE, specifically in mortgages. The effect size is material, but not 2020‑Fed‑QE material.

• The U.S. agency MBS market is in the trillions; annual gross MBS issuance runs around $1.5–2 trillion in normal times.

• A $200 billion purchase is therefore a mid‑sized one‑off demand shock, meaningful but nowhere near the Fed’s multi‑trillion QE programs.

Based on prior episodes where large official buyers stepped into MBS (Fed QE waves), a reasonable range for a program of this size is:

Primary 30‑year mortgage rates:

• Likely impact: 0.20–0.50 percentage points lower than otherwise over the life of the program, front‑loaded into the announcement and initial buying window.

• Fannie/Freddie bid up MBS prices → MBS yields fall → lenders can quote slightly lower mortgage rates while preserving spreads.

So if the counterfactual was, say, 6.75% 30‑year, this policy might drag you into the 6.25–6.5% area, assuming no offsetting move in long Treasuries and spreads.

Not nothing—but absolutely not “back to 3% mortgages.” More like a PR‑friendly nudge.

The supply problem: housing starts, construction, and why prices don’t care about your feelings.

The real fun is when “slightly lower rates” collides with “structurally anemic supply.”

Housing starts as of the latest data (delayed by prior government shutdown) are running at about 1.25 million annualized units, the lowest since the early pandemic.

Within that:

• Single‑family starts: roughly 874,000 annualized, near the low end of the last couple of years.

• Multifamily (5+ units): dropped sharply (around −25.9% month‑over‑month in the most recent report), signaling a serious cooling in rental‑oriented construction.

In other words, the construction engine is already throttled back right as demand is about to get a small rate‑driven adrenaline shot.

• Investors (all kinds, not just Blackstone‑type giants) accounted for roughly 30% of single‑family purchases through the first three quarters of 2025, the highest share on record.

• Large institutional buyers, though, have already pulled back hard; they bought only 0.3% of all homes in 2024 and have been net sellers for several quarters.

So banning “large institutional buyers” from adding more homes:

• Hits a tiny fraction of current demand.

• Leaves small investors (90%+ of investor‑owned homes) and primary buyers untouched.

Net effect on supply: basically cosmetic. You might free up a rounding‑error level of incremental inventory over time; it does not materially change years of underbuilding.

House prices: who wins when you mix lower rates with tight supply?

With supply this weak, the usual rate → price channel is brutally simple: slightly cheaper financing bids up the limited stock of homes rather than dramatically expanding access.

Assuming:

• 30‑year mortgage rates drift down 0.25–0.50% versus baseline from the MBS buying.

• Housing starts stay in the neighborhood of 1.2–1.3 million annualized, with no big policy boost to building.

Then over 12–24 months, the likely pattern is:

• Modest rebound as some rate‑locked owners finally move and marginal buyers re‑enter.

• Direction: up, not down, because more demand is chasing a fixed/slowly‑growing stock.

• Ballpark: Think low‑ to mid‑single‑digit annual price gains instead of the flat/soft scenario you might have seen under higher-for-longer rates.

So yes, it “helps” buyers in the sense of lowering monthly payments relative to an unchanged‑rates world, but it also props up or accelerates price appreciation, keeping the entry ticket high.

Inflation and macro: how this plays into the bigger mess

A $200B MBS sweep plus structurally tight housing turns into stealth support for sticky shelter inflation.

• Shelter (rent + owners’ equivalent rent) is a large share of CPI and PCE; when home prices grind higher and multifamily starts slump, the pipeline for future rent relief gets thinner.

• With multifamily construction already down sharply and investor‑owned rental portfolios not being structurally unwound, the policy cocktail leans toward keeping shelter inflation elevated rather than breaking it.

• Trump is effectively telling the GSEs to re‑lever into mortgage risk, echoing the pre‑2008 playbook that ultimately required a bailout when defaults surged.

• If the program works “too well” and re‑heats housing and shelter inflation, it could box the Fed into staying tighter elsewhere, limiting how far broader rates can fall.

Net macro read:

• Mildly stimulative for housing demand and construction margins.

• Inflationary at the margin via shelter, especially with multifamily starts getting kneecapped.

• Politically: easiest win is “look, mortgage rates are 25–50 bps lower,” while the harder truth—“and homes are even less affordable for first‑timers in 2–3 years”—gets buried in BLS tables.

.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BUY THE DIP NAVY - Limited Quantities - Grab Yours Today! CLICK HERE

BUY THE DIP NAVY…

Thank you for reading, we appreciate your feedback—sharing is caring.

Reply