- The C.R.E.A.M. Report

- Posts

- AI The Silent Economy Crasher...

AI The Silent Economy Crasher...

Want to Blow Bubbles...

Kevin Davis

March 10, 2026

Above Average Info For The Average Joe…

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - WEALTHY RED - Limited Quantities - Grab Yours Today! CLICK HERE

WEALTHY RED…

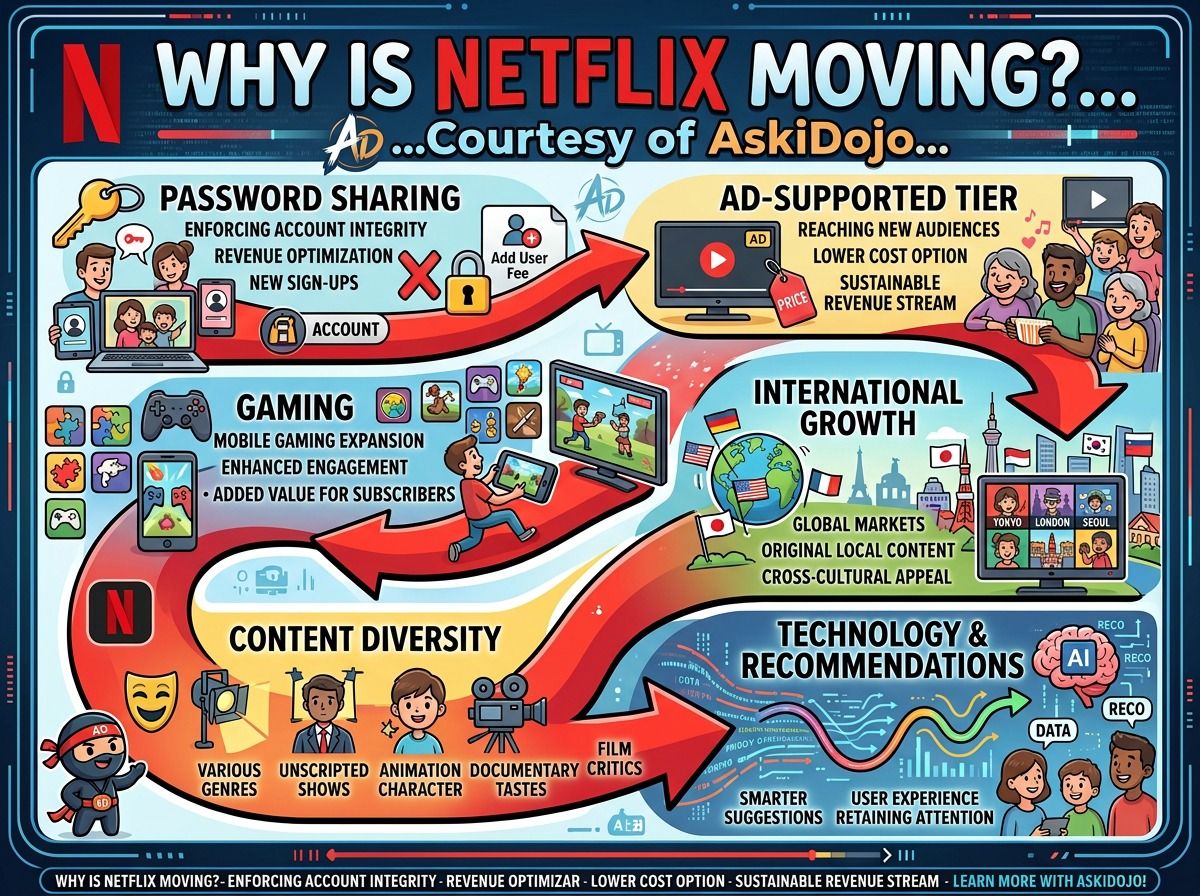

Why Is Netflix Moving?…Courtesy of AskiDojo…

🎯 PRIMARY DRIVER

NFLX's -0.15% decline aligns precisely with the Streaming industry average (-0.15%), driven by sector-wide sentiment drag from PARA's -6.04% plunge rather than company-specific catalysts.:No breaking NFLX news today; recent M&A like the March 5 acquisition of InterPositive shows positive momentum.

📰 CURRENT NEWS & NARRATIVE

Markets closed for the weekend (last session Friday, March 6, 2026). NFLX closed at $99.02, down -0.15%, with after-hours dipping to $98.41 (-0.61%). Recent headlines include Netflix acquiring Ben Affleck's AI startup InterPositive on March 5 (positive M&A signal); PSKY winning WBD bidding war over NFLX (minor competitive loss, 8h ago); and optimistic takes like "Is Netflix Stock Going to $150?" (22h ago) plus buy reasons post-Blockbuster bid (27h ago).[company context] Institutional buying noted: Milestone Asset Management added 6,546 shares, WP Advisors added 23,770 shares (recent filings). No fresh breaking news today; narrative remains bullish on AI/growth amid neutral consensus.

🌍 GEOPOLITICAL & MACRO FACTORS

No specific geopolitical events (tariffs, trade tensions, or regulations) targeting Communication Services or Streaming this week. Broader macro pressure from Friday's session: SPY -1.31%, QQQ -1.50%, with XLK -2.06% (tech drag spilling over).[macro] Fed policy or rate expectations not cited as direct NFLX factors; sector up +0.18% overall despite rotation out of tech/comm names.

📊 ANALYST ACTIVITY

No upgrades, downgrades, or price target changes in the last 48 hours. Consensus remains Neutral (3/5 score), with average price target $510.57—implying ~416% upside from $99.02 (noted as of March 6). First Trust Advisors holds $892M position (37h ago).[company context]

🔄 SECTOR DYNAMICS

Communication Services +0.18% vs. sector avg move -1.17% (conflicting data suggests intraday volatility).[sector] Streaming industry exactly matching NFLX at -0.15% avg, confirming no outperformance/underperformance. NFLX +1.02% relative to sector avg, but inline with peers. Sympathy drag from PARA -6.04% (major sector catalyst, likely media sentiment hit); other losers META -2.38%, RBLX -3.86%. Gainers CHTR +1.00%, CMCSA +0.98% show cable/trad media resilience. Money flowing to defensives (XLP +0.43% best sector); Streaming lagging tech (XLK -2.06%).

⚡ ACTIONABLE TAKEAWAYS

●Bull Case: Recent AI M&A (InterPositive acquisition March 5) and institutional accumulation signal growth; $510 target supports re-rating if PARA noise fades.

●Bear Case: Prolonged PARA/WBD drama erodes Streaming sentiment; volume 0.82x avg hints low conviction, vulnerable to tech rotation.

●Watch For: Monday open reaction to weekend news; key levels $98 support (after-hours low), $100 resistance; Q1 2026 earnings buildup.

🚀 BOTTOM LINE

This -0.15% dip is pure sector/industry noise—NFLX tracking Streaming peers amid PARA's outsized -6.04% sympathy hit, not company-specific weakness. Signal over noise: Buy the institutional flows and M&A momentum; relative outperformance (+1.02% to sector) positions NFLX as Streaming leader heading into 2026.

JOIN THE WAITLIST ASKIDOJO.AI/LAUNCH

If Second Guessing Yourself Were A Sport…

Every bull market has its heroes, its geniuses, and its legends in the making. Every bear market has… Second Guessing Dan.

You’ve seen him before. He’s the guy pacing in front of his trading app like it’s a slot machine that owes him money. The stock market, to Dan, is not an ecosystem or a long-term wealth engine. It’s a mood ring. When it’s green, he’s euphoric.

When it’s red, he’s clinically unwell. Dan doesn’t really watch the market; the market watches him — and it moves accordingly.

Dan is a high-maintenance investor, which is a polite way of saying he’s allergic to conviction. He checks his portfolio like a hypochondriac checks WebMD. Every downtick is a new symptom. Every pullback a potential terminal illness.

He doesn’t believe in his choices — not really. When he buys a stock, it’s not because he’s modeled cash flows or studied industry dynamics. It’s because Jim Cramer yelled about it, or because it was trending on social media next to a rocket emoji.

But Dan doesn’t see himself as impulsive — oh no, he calls it “nimble.”

He’ll tell you that the market changes fast, and you’ve got to move with it. He’ll also tell you he’s “protecting capital,” which is Dan-speak for “I got scared and sold at the low again.”

This is why institutions love Dan. He is everything they dream of: predictable, emotional, and 100% convinced he’s in control.

Unbeknoweth to Dan, he Is the Entrée. Dan thinks he’s trading against other people like himself, but in reality, his counterparties aren’t sitting in their pajamas behind a trading app. They’re institutions armed with teams of PhDs, industrial-grade data feeds, and enough computing power to simulate global market sentiment before Dan can even open his phone.

When Dan “feels good” about a stock, it’s usually because the algorithms made him feel that way — because they’ve already extracted their slice of optimism from retail flows.

Example: the market turns green one Friday afternoon. Dan, watching in awe, says to himself, “I knew this would rip!” He nukes his cash position, buying near the peak. Monday morning, the same market gaps down 3%. His stomach sinks. It’s not the loss that stings; it’s that he didn’t see it coming again.

This is not bad luck. This is design. Algorithms now trade based on the collective behavior of investors like Dan — the predictable rhythm of fear and greed that pulses through retail platforms every time volatility spikes. In other words, Dan’s emotions are a data set.

Hedge funds don’t need to guess what he’ll do next. They already know.

Ask Dan about macroeconomics and he’ll give you the full emotional weather report:

“The Fed’s out to get us,” “Oil’s going crazy again,” and “This Ukraine thing is really going to tank my portfolio.”

Dan confuses events in the world with events aimed at him. He watches CNBC not to understand but to validate the drama. When inflation ticks up, it’s a personal attack. When the market rallies without him, it’s rigged.

If you mention the business cycle, he’ll say, “Yeah, recessions are bad for me.” If you mention liquidity, he’ll say, “I don’t mess with crypto.” If you mention the yield curve, he’ll blink like you just spoke in whale song.

Meanwhile, the pros — those same “evil institutions” — are looking at multi-decade data, capital flows, and risk metrics. They move in quarters, not seconds. They use the kind of math that would make your high school teacher cry.

To them, Dan isn’t unpredictable chaos. He’s liquidity. He’s part of the market’s digestion process — a calorie to keep the system running. Every time Dan panics, sells low, and buys high, some quant’s quarterly bonus gets a little fatter.

Let’s not sugarcoat it. Dan is outgunned.

He’s a man with a smartphone trying to outmaneuver machine-learning systems that analyze terabytes of data per minute.

He’s using gut instinct in a war of nanoseconds.

Consider what stands against him:

• High-frequency trading firms shaving partial cents off spreads through co-located servers sitting closer to the exchange backbone than Dan’s entire Wi-Fi router chain.

• Quant funds that model market behavior using neural networks trained on decades of tick data.

• Institutions using satellite imagery to count retail parking lots, scrape corporate filings for sentiment, or analyze shipping manifests to front-run earnings.

Dan, meanwhile, is refreshing his Robinhood app and checking Reddit for “confirmation.”

In the arms race of modern finance, Dan shows up barefoot. But the cruel joke — and it’s a darkly funny one — is that he doesn’t have to lose. In fact, he could win. But he won’t, because the greatest enemy of Second Guessing Dan isn’t the institution…it’s Dan.

If you strip away the jargon and technology, there’s still one thing retail investors can do that no hedge fund can match: hold for the long term.

An algorithm can’t sit quietly through drawdowns. Its capital gets pulled or rebalanced. Hedge funds can’t wait ten years; they’d be lucky to survive two bad quarters.

But an individual investor could — if he learned to shut up and sit still.

The hardest part? Convincing Dan that doing nothing is an actual strategy. Dan believes that in order to be “active,” he must constantly prove he’s paying attention. But the market doesn’t reward attention. It rewards patience.

If Second Guessing Dan simply bought quality businesses — or even a boring index fund — and then stopped logging in for a few years, he’d outperform most of the caffeinated geniuses in Manhattan.

But that’s not who he is. He’ll chase when it’s up, hide when it’s down, and always insist he’s “learning from it this time.” As the old saying goes: “Buy when there’s blood in the streets.” For Dan, that only makes sense when it’s someone else’s blood.

The moment he sees red in his own portfolio, he’s gone — offloading his positions to the very same institutions who set the emotional trap in the first place. So every month, like clockwork, the market extracts its tax from Dan — not in dollars, but in dopamine and despair.

In the grand ecosystem of finance, he has a purpose. He is nourishment.

The pros call it volatility harvesting. The cynical call it what it is: taking candy from a baby.

Maybe one day Dan will learn. Maybe after his fifth “sold too early” and sixth “got back in late,” he’ll realize that the trick to surviving the markets isn’t outsmarting them; it’s outlasting them.

But more likely, he’ll just tweak his strategy again, download a new trading app, and tell his friends that this time, it’s different.

The truth is, everything that happens — every bounce, every crash, every rally — doesn’t happen “to” Dan. It happens because of Dan.

He is both participant and product. The market doesn’t eat him by accident. It eats him because he tastes so good. And that, dear readers, is why Second Guessing Dan remains the market’s favorite snack.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BILL GATES BLACK - Limited Quantities - Grab Yours Today! CLICK HERE

AI The Silent Economy Crasher…

Killer…Inflation isn’t just rising prices; it’s the slow, quiet realization that your job was the thing being inflated away – and AI just popped it.

What follows is “The Stack: The Inflation No One Saw Coming” – a cynical tour through how artificial intelligence can hollow out workers, tax bases, and social stability faster than voters or policymakers can learn what a prompt even is.

The spark: Block just showed you the endgame

Block just announced it’s firing roughly 4,000 people – about 40% of its workforce – explicitly because AI means it can do the same work with fewer humans. Jack Dorsey’s line is simple: “intelligent tools” let a much smaller team “achieve more and do it more effectively,” and investors cheered as the stock ripped higher.

This is the script:

• AI adoption, big productivity gain, big headcount cut, stock up, executives hailed as visionaries.

• Younger and entry‑level workers get hit first; Stanford research finds AI‑exposed sectors have already been cutting more junior roles since around 2024.

• CEOs openly say they expect AI to eliminate huge swaths of white‑collar work; Anthropic’s CEO has floated scenarios where up to half of entry‑level white‑collar jobs vanish within five years and unemployment could spike into the 10–20% range.

Block is not a one‑off accident; it’s the template that tells every board: “You’re overstaffed if you’re under‑automated.”

The consumer is about 70% of U.S. GDP; that’s not a slogan, that’s the thin plank the whole system is standing on. Traditional inflation is prices outpacing wages; AI inflation is productivity outpacing employability.

Three nasty feedback loops:

• Wage erosion loop: If AI allows output to grow with fewer workers, wages and bargaining power stagnate or fall even if GDP looks “fine.”

• Confidence shock loop: Consumers who fear job loss save more, spend less; economists already warn that AI‑driven job cuts are a major downside risk to U.S. growth over the next few years because consumption slows.

• Inequality pressure cooker: AI and automation tilt income toward capital owners; research on OECD and U.S. data shows the labor share of national income has weakened, especially in the United States.

Here’s the part people don’t want to say out loud: you can have healthy corporate earnings, solid headline GDP, and a stock market on fire while a generation of younger workers gets structurally sidelined. The average doesn’t care that it’s built on an underemployed underclass.

Government is funded mostly by taxing people who work – wages, payrolls, and their spending – not GPUs. If AI steadily replaces labor with capital, the tax base quietly shifts from something we tax heavily (labor) to something we tax lightly (capital, automation, software).

Researchers in labor economics and tax policy warn of three collision points:

• Declining labor share: As automation makes workers less central in production, wage income shrinks relative to profits, especially in the U.S.

• Eroding tax base: Because advanced economies depend heavily on labor and payroll taxes, automation that replaces workers “all else equal” means tax revenues fall unless rates or structures change.

• Perverse incentives: Current tax systems often favor automation over employment through deductions and incentives, effectively subsidizing the decision to replace humans.

A few examples show policymakers see the problem but barely touch it:

• South Korea didn’t “tax robots,” but it became the first country to dial back tax incentives for automation in an effort to slow job displacement.

• Academic and policy papers argue that taxing robots or AI at least at the same effective rate as labor could reduce distortions and limit inequality, but they also note political and competitiveness risks if only one country moves first.

If the U.S. automates hard without re‑architecting taxes, you get a scenario where:

• Corporate profits and capital gains soar;

• Income and payroll tax receipts stagnate or fall;

• Demands for social spending explode as more people rely on safety nets;

• The gap is filled by deficits until bond markets or politics flinch.

The punchline: automation without tax reform is effectively a stealth austerity plan aimed at the people being automated out.

The supposed comfort is that “AI will create new jobs.” Long‑term, maybe. Short‑term, the timing mismatch is lethal for younger workers.

Current data and surveys paint a stark picture:

• International surveys show about 70–80% of firms in advanced economies already use some form of AI, especially in the U.S., UK, and Germany.

• Over 80% of firms say AI has not yet significantly changed employment or productivity – suggesting we’re still early in the curve.

• But when firms look three years out, they expect AI to increase productivity and output while reducing employment by around 0.7% on average.

That sounds “modest,” until you remember:

• The cuts are not evenly spread; they cluster in tasks that are routine, codifiable, and common in entry‑level and junior jobs.

• Stanford‑linked work and CEO surveys both suggest early impacts show up first in younger, less experienced workers, exactly where you’re supposed to be climbing the ladder.

You can’t “retrain” a 24‑year‑old out of a job that no longer exists as an on‑ramp. If AI kills the apprenticeship layer – the lower‑risk, lower‑pay jobs where humans learn – you don’t just get more unemployment; you get an entire cohort that never builds the skills to compete at the new “AI‑complement” level.

What it would take to catch up (and why we probably won’t)

In theory, we know roughly what it would take for society to catch up to the AI learning curve instead of being flattened by it:

• Massive, early, and repeated reskilling: You’d need large‑scale programs teaching AI‑complementary skills (prompting, data reasoning, domain expertise, hands‑on technical skills) starting in high school and continuing through adulthood.

• Active labor market policies: Subsidies for firms that retain and retrain workers instead of firing them; wage insurance; support for geographic and occupational mobility.

• Tax realignment: Shifting part of the tax burden from labor to capital and automation – for instance by reducing payroll taxes while raising effective taxes on highly automated profits – to keep revenues stable without punishing employment.

• Transitional income floors: Some mix of expanded unemployment benefits, negative income taxes, or targeted basic income pilots for regions and sectors where AI displacement hits hardest.

This is the wishlist. The reality:

• Most countries are still arguing about whether to talk about “robot taxes,” while companies are rolling out AI stacks on quarterly timelines.

• Training and education systems move on decade cycles; AI models move on 6–18 month cycles.

• The political constituency for the displaced doesn’t exist yet because they’re still clinging to jobs that are quietly being set up for elimination.

Cynically: it will probably take a visible, sustained spike in unemployment among younger workers and a tax‑revenue scare before serious structural reforms even get on the ballot. By then, the gap between the AI‑complement “winners” and everyone else will be baked in.

Scenarios to keep you up at night

Here are three plausible paths – none of them mutually exclusive.

Scenario | Core Dynamic | Who Wins | Who Loses |

|---|---|---|---|

Slow-burn squeeze | AI raises productivity modestly, firms trim headcount slowly wages stagnate, tax base erodes over decades | Capital Owners, large AI-intensive firms, top skillid workers | Younger and mid-skill workers, local goverments, welfare systems |

Shock wave | A few big players ( finance tech, customer service ) follow Block aggressively: unemployment jumps: consumption stalls; recession risk rises | Early adopters with strong balance sheets: investors who front-ran the cuts | Newly unemployed white-collar workers small businesses tied to their spending |

Policy whiplash | Populist backlash leads to rushed “robot taxes” AI moratoria or proctectionist rules: firms delay hiring and capex: growth weakens further | Incumbents with lobbyists and cash to nativigate complex regulation | Startups, workers in countries that move alone and lose investment |

In every scenario, if you don’t design deliberate programs to absorb and redeploy displaced workers, you drift toward a society where:

• A shrinking slice of highly skilled humans and AI systems produce most value;

• The majority live on a mix of low‑wage service work and transfer payments;

• Politics increasingly revolves around how to tax a narrow, mobile capital base to fund a large, immobile population.

That’s the real “inflation no one saw coming”: not CPI, but the inflation of obligations – pensions, healthcare, social support – against a tax base that’s being quietly automated away.

Corporate America has already answered the question “Will AI replace workers?” It answered it with a 4,000‑person layoff and a 20% pop in one company’s stock. Policymakers, by contrast, are still holding panel discussions about “inclusive growth in the age of AI” while tax codes quietly subsidize the very automation that will undercut their future revenues.

If you’re a younger worker, the uncomfortable truth is this: the system is currently optimized to reward your employer for replacing you with software, not for helping you outrun it. The only real question is whether society rewrites the rules fast enough – taxes, training, safety nets – or whether you discover, the hard way, that the job wasn’t the only thing AI was automating. It was your bargaining power, your tax contribution, and ultimately your place in the economy.

WHEN INVESTING BECOMES A LIFESTYLE YOU WEAR IT!

NEW MERCH ALERT - BUY THE DIP NAVY - Limited Quantities - Grab Yours Today! CLICK HERE

BUY THE DIP NAVY…

Quick Links…

Wanna Smoke…

Now We Are All Doomed…

The Markets Are Changing…

Thank you for reading, we appreciate your feedback—sharing is caring.

Reply